Making Financial Literacy Shareable: Social Formats That Turn Education into Engagement

Financial services are in the middle of a trust reset. Younger consumers are no longer defaulting to banks, advisors, or institutions, they’re turning to decentralised, creator-driven communities instead. As of early 2025, over seven in ten Gen Z consumers and nearly the same proportion of Millennials say social media has a positive impact on their financial decisions. This is not a niche behaviour, it represents a structural shift in how financial literacy is formed and applied.

For financial brands and educators, the challenge is clear: how do you transform dense, intimidating topics into shareable assets that trigger engagement without sacrificing accuracy? Getting this right is now central to finance marketing: firms must master the intersection of cognitive psychology, social-first formatting, and rigorous regulatory standards to own the digital conversation.

The Socio-Digital Evolution of Money Talks

Traditional models of financial education often suffered from high barriers to entry, including jargon-heavy delivery and intimidating professional settings. In contrast, “FinTok” and its cross-platform equivalents have democratised access through approachable narratives. By 2025, the average FinTok user was spending over 400 hours annually scrolling through financial content.

Crucially, this engagement isn’t limited to younger cohorts. Data indicates that even Baby Boomers consume an average of 32 pieces of financial advice annually on TikTok. The search behaviour within these communities reveals a high demand for core digital banking topics, with “Budgeting and Saving” leading search frequency at 25%, followed closely by “Investing Strategies” at 24%. Since 44% of users successfully implemented a financial trend they discovered on social media in 2024, these platforms now act as high-intent funnels for real-world behaviour change.

The Psychology of the Share: Why We Click

The transition from education to engagement is driven by specific psychological mechanisms. Neuroscience suggests that curiosity-driven learning stimulates the brain’s reward system, increasing dopamine release in the ventral striatum and hippocampus, which significantly enhances memory formation.

1. The Curiosity Gap and Information-Gap Theory

A primary driver of engagement is the curiosity gap. Derived from Loewenstein’s Information-Gap Theory, this drive state is triggered when an individual detects a discrepancy between their current knowledge and a desired understanding. For financial content, this means presenting a surprising or counterintuitive fact to create cognitive tension that the user seeks to resolve by consuming the rest of the asset.

The sweet spot for maximal curiosity lies at a moderate knowledge gap. If a topic is too familiar, curiosity remains dormant; if it is entirely alien, the user lacks the context to recognize what is missing. Effective designers tease without revealing, using techniques like showing a 92% match or a cryptic preview of a money breakthrough while withholding the core mechanism until the climax of the video or post.

2. The Zeigarnik Effect and Narrative Tension

Humans remember uncompleted tasks better than completed ones. By using progress bars or cliffhanger hooks, creators can leverage the Zeigarnik Effect to keep users engaged through a multi-step educational series. Furthermore, patterning content with tension-and-release cycles, building stress (e.g., the fear of debt) and providing immediate, actionable resolution, mirrors the satisfying structures of musical composition.

3. Cognitive Ease and Processing Fluency

While curiosity attracts the user, cognitive ease, the preference for things that are easy to think about, determines if they stay. Content that uses clear language, clean design, and logical organisation is perceived as more trustworthy. The brain seeks information efficiency, favouring content that provides maximum value with minimum cognitive load. This necessitates information chunking, breaking complex wealth-building strategies into bite-sized, sequential lessons.

High-Engagement Financial Formats for 2026

The efficacy of financial education is intrinsically linked to its format. As we progress through 2026, several specific mediums have emerged as the dominant drivers of engagement.

Short-Form Vertical Video (TikTok, Reels, Shorts)

Short-form vertical video is the #1 driver of viral performance. Completion rates for financial content under 30 seconds average over 68%. Algorithms reward watch time and rewatch rates, meaning fast-paced videos with text overlays and trending audio perform 2-3x better than standard feed posts. For financial brands, the shift toward authentic beats polished is critical; spontaneous, informal videos resonate more deeply with an audience seeking relatability.

Carousel Posts and Dwell Time

Carousels are among the most shareable formats on Instagram and LinkedIn. Each swipe is a micro-commitment that signals to the algorithm that the content is valuable.

- The Structure: Optimal carousels typically employ 5-7 slides. Slide 1 is the gateway, a bold statement or provocative question like “What’s your £10,000 LinkedIn mistake?”.

- The Visual Hierarchy: Since most users browse on mobile, carousels must use large, legible fonts (minimum 24pt for body, 36pt+ for headers) and keep key elements centred to avoid unintended cropping in the grid view.

- The Payoff: LinkedIn carousels that maintain a completion rate of over 60% are favoured by ranking factors, making it essential to resolve the curiosity gap only in the final slides.

Getting that visual hierarchy and pacing right consistently, across dozens of slides a month, is exactly the kind of disciplined execution a social media content agency is built for.

“This vs. That” and Comparative Storytelling

Comparative formats are highly effective for teaching critical thinking. By comparing two options, such as an expensive £38 moisturiser vs. an £8 budget alternative, or a High Interest Savings Account vs. an Index Fund, creators encourage organic discussion in the comments. These comparisons often use metaphors like green flags vs. red flags or what people think happens vs. what actually happens to simplify complex professional audits.

Transforming Financial Math into Social Narratives

To bridge the gap between institutional accuracy and social engagement, marketers must adopt frameworks that prioritise the consumer’s emotional journey.

The “Aha!” Moment

The “Aha!” moment is the point at which a user first realises the value of a financial concept. Scientific studies on insight learning show that these sudden realisations result in a temporary increase in risk preference and confidence. For example, presenting the “Rule of 72” not as a dry formula, but as a wealth secret for doubling your money, creates a positive affect that can be funnelled into opening a brokerage account.

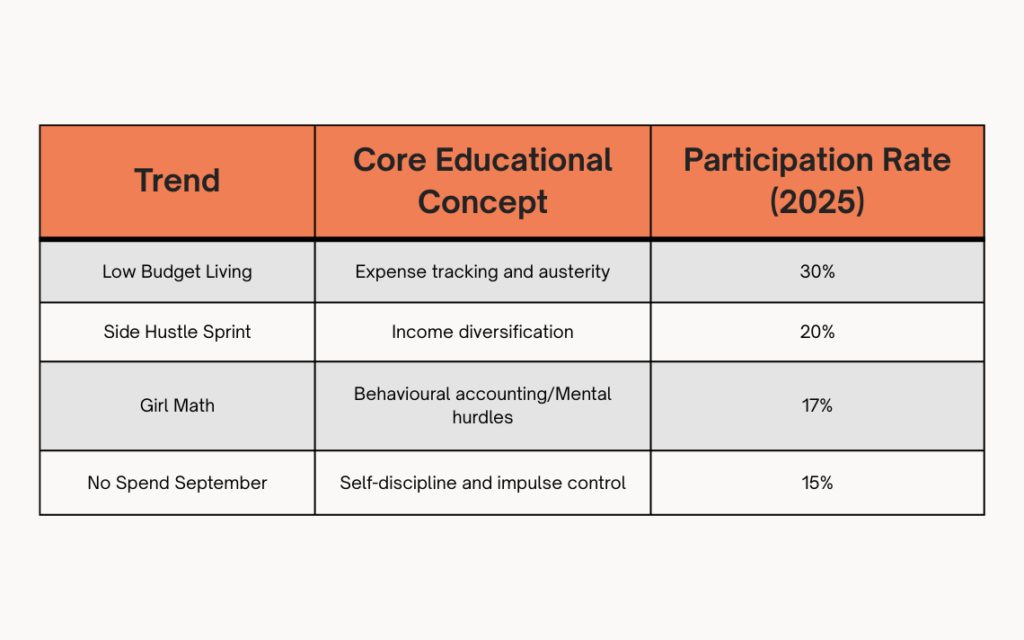

Trend-Driven Education

FinTok trends act as gateway topics. The top trends of 2024-2025 have directly impacted consumer behaviour, leading to an average of $400 in savings for participants.

Trends like “Loud Budgeting”, which involves vocalising money goals to friends and family to ensure accountability and combat the shame many feel regarding their spending habits.

Strategic Persona Mapping

A one-size-fits-all approach is ineffective in the fragmented social landscape. Successful content must be segmented by persona cohorts that reflect specific life-stage triggers.

- The Young Professional (Alex): Age 32, tech-savvy. Alex prioritises quick, digestible content like podcasts and investment calculators to manage risk.

- The Small Business Owner (Kevin): Struggling with compliance. Kevin needs practical how-to guides on efficient bookkeeping and avoiding common accounting mistakes.

- The Retirement Planner (John and Mary): Middle-aged couple concerned with healthcare costs. They respond well to interactive tools, webinars, and comprehensive roadmap guides.

- The High-Net-Worth Individual (Sarah): Interested in wealth protection. Sarah responds to case studies showing real-world examples of strategic tax reduction.

Navigating the Financial Regulatory Landscape

The democratisation of advice via finfluencers has triggered a significant regulatory response. Financial promotions on social media are now subject to strict scrutiny to ensure they are fair, clear, and balanced.

The FCA Business Test (UK)

The Financial Conduct Authority (FCA) guidance FG24/1 clarifies that social media posts are subject to financial promotion restrictions if they are made in the course of business. This applies if an influencer has a commercial interest, such as receiving payment, commission, or even a revenue-sharing agreement with a platform.

- Standalone Compliance: Every individual post must comply with rules on its own merit; users should not have to click through a thread to find a risk warning.

- Prominent Warnings: For High-Risk Investments (HRIs), risk warnings must be displayed prominently throughout the promotion and cannot be obscured by platform features like see more buttons.

FINRA Oversight (US)

In the US, FINRA mandates that firms supervise all business-related social media communications. A registered principal must review any site a representative intends to use for business before use to ensure compliance with rules against false or misleading claims. Furthermore, firms must retain records of these communications for at least three years.

Institutional Implementation: Case Studies in Financial Success

Transitioning to a social-first strategy requires a recalibration of the marketing department from transactions to edutainment.

1. Monzo’s Community-Centric Strategy

Monzo’s success is rooted in emotional resonance. By designing rituals for savings and round-ups, they turn financial progress into an everyday habit. Their “Book of Money” campaign enlisted 12 creators to share personal insights on shifting their financial mindsets, achieving 12.8 million views and nearly 100,000 engagements.

2. SoFi and Journalistic Storytelling

SoFi transformed its digital presence by moving away from product-focused SEO blogs toward long-form member spotlights and debt management stories. This revamped approach turned casual browsers into engaged community members, resulting in a 970% increase in site traffic and a 247% increase in monthly conversions.

3. BlackRock’s Humanised Narratives

BlackRock struck content gold with “How the World Retires,” an interactive report profiling the retirement journeys of six global couples. By combining vivid photography with a nifty retirement calculator, the report outperformed the average BlackRock post by sixfold.

4. Julius Baer and Employee Advocacy

Julius Baer enlists a content partner to create advocacy materials for employees to share on LinkedIn. This global initiative resulted in 5.3 million impressions, with the reach of its 350 brand ambassadors growing to more than double that of the official brand channel.

These examples make the same point: in a sector this regulated, the trust of a real person’s voice still travels further than a brand account, which is why a specialist influencer marketing agency is increasingly part of the financial marketing mix, not just a consumer brand tactic.

Conclusion – The Future: Toward the “Financial OS”

In 2026, leading digital providers are competing to become the “Financial OS” for their users. This concept involves a platform that doesn’t just manage transactions but guides users through major life moments, getting a first job, getting married, or buying a home.

The future of shareable financial literacy lies in:

- Intelligent Orchestration: Using behavioural signals to adjust suggestions based on travel and spending patterns.

- Assurance-Based Marketing: Moving from delight-based to assurance-based operations, where brands become the first port of call for safety and certainty in an unstable economy.

- Hybrid Learning: Sponsoring financial education in schools to build early trust in a controlled setting, which then transitions into social-first adult learning.

Institutions that embrace these shifts, prioritising relatability, accessibility, and digestibility, will establish themselves as the trusted authorities of the digital age, effectively turning education into lasting engagement. It’s the same principle behind good social media marketing services more broadly: meet people where the trust already lives, and the engagement follows.

See how we can support you, get in contact with us today!